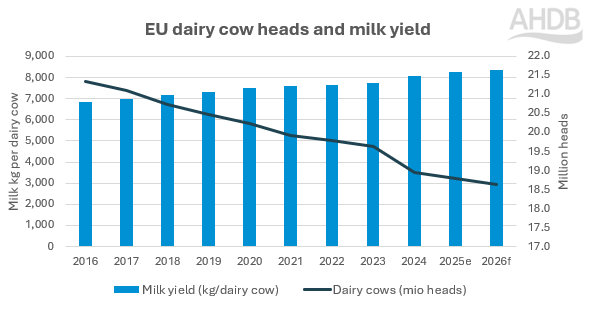

The European Union dairy sector is navigating a delicate transition phase as the unexpected production surge seen last year begins to cool. According to the European Commission’s Spring 2026 Short-Term Agricultural Outlook, raw milk prices across the bloc are showing early signs of stabilisation following a sustained downward correction that commenced in October 2025. While total EU milk production is projected to edge up by a marginal 0.2% over the entirety of 2026, this growth is heavily front-loaded. A strong first-quarter expansion is expected to give way to a year-on-year contraction in supply during the second half of the year, reshaping global export availability and creating strategic openings for competing dairy-producing nations.

Processing Arrays Realign as Liquid Volume Sours

The structural landscape of European dairy processing is undergoing a deliberate pivot. Caught between shrinking domestic liquid milk consumption and robust international demand for premium components, processors are channelling an increasing share of the milk pool into high-value-added portfolios.

Cheese and whey derivatives remain the primary beneficiaries of this structural realignment. Backed by resilient domestic consumption and solid export demand, cheese production is forecast to expand further through 2026. Conversely, commodities tied to lower-margin profiles or suffering from uncompetitive pricing structures face a structural retreat.

| Dairy Product Category | 2026 EU Production & Export Outlook | Primary Market Drivers |

| Cheese & Whey | Expanding production and export volumes | Robust domestic demand; strong global appetite for nutritional lipids and proteins |

| Skimmed Milk Powder (SMP) | Stable production; steady export volumes | Enhanced structural competitiveness following the sharp corrections of 2025 |

| Butter | Output flattening after a high 2025 baseline | Prices are stabilising after hitting historic post-pandemic lows in late 2021 |

| Whole Milk Powder (WMP) | Persistent decline in production and exports | Severe structural price uncompetitiveness; collapsing demand in traditional destination markets |

The continuous decline in Whole Milk Powder output underscores Europe’s broader challenge in balancing high farmgate operating costs against cheap international alternatives. Meanwhile, fresh liquid drinking milk volumes continue their long-term downward trajectory, though the fresh category finds partial cushion in rising consumer demand for yoghurt and cream.

The India Angle: A Strategic Opening for Value-Added Protein

For the Indian dairy sector, the structural tightening of the EU milk pool and its shift away from basic powders carry major strategic implications. Historically, India and the EU have operated in largely insulated spheres due to strict sanitary and phytosanitary barriers. However, the current transformation in European processing is changing the competitive dynamics of global trade.

Strategic Takeaway: As European processors aggressively divert their raw milk supply into cheese and whey derivatives to satisfy global nutrition and lifestyle trends, a supply vacuum is emerging in mid-tier skimmed milk powder and whole milk powder export markets across South and Southeast Asia.

Indian dairy cooperatives and private processors, currently upgrading their capacities to manufacture high-quality, export-compliant ingredients, have a distinct window of opportunity. While domestic liquid milk demand within India absorbs the vast majority of local production, matching the export competitiveness of a leaner EU SMP market is increasingly feasible. Furthermore, as the EU shifts its focus towards specialised whey fractions, Indian functional food and muesli brands seeking premium domestic alternatives may have strong fiscal reasons to support localised ingredient supply chains.

Supply Friction Ahead

Looking toward the horizon, the second half of 2026 will test the resilience of European dairy margins. Farmgate input costs, though down from the hyperinflationary peaks of 2022, remain elevated across core operational variables, including specialised labour, fuel, and regulatory compliance. The initial cushion provided by cheap compound feed is wearing thin as dairy herd culling rates accelerate in major countries such as Germany and France.

If global demand from key deficit regions experiences even a modest macroeconomic recovery in the final quarters of the year, the combination of a shrinking EU herd and lower late-season milk flows will exert sharp upward pressure on global physical commodity prices.