Global dairy trade has continued its steady expansion despite market disruptions, growing by 11% between 2017 and 2025 to reach 101.2 billion kilograms in liquid milk equivalents (LME), according to the latest Rabobank Global Dairy Trade Report. The report highlights how changing consumer demand, evolving export strategies and the growing importance of value-added dairy products are reshaping the international dairy market.

While overall trade continues to expand at a long-term average growth rate of around 2% annually, the report notes that 2025 recorded a stronger 5% increase, recovering from slower growth in 2024 and the supply disruptions experienced in 2022 following a sharp decline in New Zealand’s milk production.

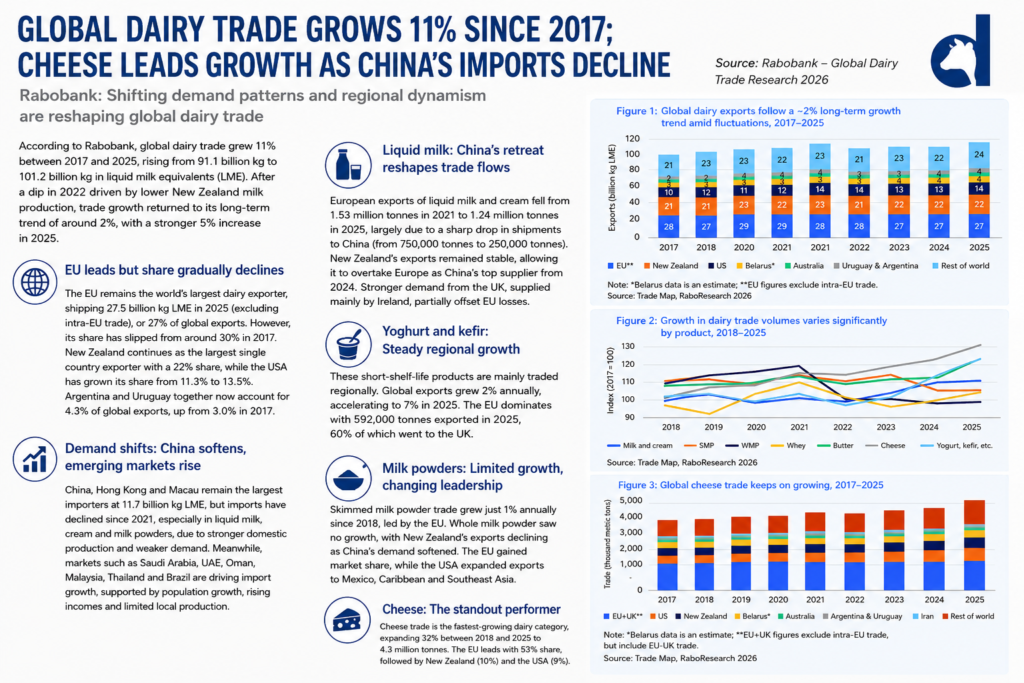

EU Retains Leadership as Global Dairy Export Landscape Evolves

The European Union remains the world’s largest dairy exporter, shipping 27.5 billion kg LME in 2025, accounting for approximately 27% of global dairy exports, excluding intra-EU trade.

However, Rabobank notes that Europe’s dominance is gradually declining. The region’s export share has fallen from nearly 30% in 2017, while other exporters continue to strengthen their global presence.

New Zealand remains the world’s largest individual country exporter with a 22% market share, while the United States continues to expand rapidly, increasing its share of global dairy exports from 11.3% in 2017 to 13.5% in 2025.

Argentina and Uruguay have also strengthened their position, jointly accounting for 4.3% of global dairy exports, reflecting increasing competition in international dairy markets.

China’s Import Slowdown Reshapes Global Dairy Demand

The report identifies one of the most significant structural shifts in global dairy trade: the gradual decline in Chinese dairy imports.

Although China, together with Hong Kong and Macau, remains the world’s largest dairy importer with 11.7 billion kg LME, imports have steadily declined since reaching their peak in 2021.

Rabobank attributes the slowdown to increased domestic milk production and softer consumer demand, particularly for liquid milk, cream and milk powders.

As China’s demand moderates, exporters are increasingly targeting alternative growth markets.

Countries across the Gulf region, including Saudi Arabia, the United Arab Emirates and Oman, are becoming increasingly important import destinations due to limited domestic milk production and rising dairy consumption.

Similarly, Southeast Asian markets such as Malaysia and Thailand continue to record steady import growth, while Brazil has emerged as one of the fastest-growing dairy importers, driven primarily by rising demand for cheese and milk powders.

Liquid Milk Trade Faces Changing Dynamics

Rabobank highlights that the reduction in Chinese imports has significantly impacted European exports of liquid milk and cream.

European exports declined from 1.53 million tonnes in 2021 to 1.24 million tonnes in 2025, largely due to lower shipments to China.

Meanwhile, New Zealand maintained relatively stable export volumes, allowing it to become China’s leading liquid milk supplier from 2024 onwards.

The report also notes that growing exports to the United Kingdom have partially offset Europe’s reduced sales to China.

Milk Powder Markets Remain Under Pressure

Unlike other dairy categories, skimmed milk powder (SMP) continues to experience limited global trade growth.

Global SMP exports increased by just 0.5% in 2025, reflecting subdued international demand despite improved milk availability across exporting regions.

Whole milk powder (WMP) trade has also remained relatively flat.

New Zealand continues to dominate this segment with approximately 53% of global exports, while the European Union has gradually shifted milk utilisation towards higher-value dairy products, including cheese and butter.

Butter Exports Receive Major Boost from the United States

Global butter trade experienced a notable rebound during 2025, with export volumes increasing by 9% to approximately 2.23 million tonnes.

Rabobank attributes much of this growth to the United States, where butter exports nearly tripled within a year due to increased domestic milk availability and improved international price competitiveness.

European butter exports remained comparatively stable despite higher milk production, reflecting processors’ continued focus on manufacturing products with greater value addition.

Cheese Continues to Lead Global Dairy Trade Growth

Among all dairy commodities, cheese remains the strongest performer in global trade.

Rabobank reports that global cheese exports reached 8.96 billion kg in 2025, representing an impressive 40% increase since 2017.

The report highlights cheese as the fastest-growing dairy export category, supported by robust international demand and increasing production in major exporting regions.

Both the United States and Argentina have doubled their cheese exports during the period, while the European Union continues expanding cheese production despite relatively modest milk production growth.

The findings underline an ongoing industry trend in which processors increasingly prioritise higher-value dairy products over commodity ingredients, reinforcing cheese’s position as one of the most profitable segments within the global dairy industry.

Whey and Casein Continue Their Strategic Growth

Although whey trade volumes have remained relatively stable, Rabobank notes that the ingredient’s market value is rising rapidly.

Growing demand from the sports nutrition sector and increased use in high-protein diets associated with weight management are strengthening whey’s long-term commercial prospects.

Casein exports also continued their steady expansion during 2025, with the European Union narrowly surpassing New Zealand as the world’s largest exporter in a relatively balanced global market.

Outlook

Rabobank concludes that while global dairy trade continues to follow a steady long-term growth trajectory, the composition of international demand is changing rapidly.

The decline in Chinese imports, rising consumption across emerging economies, growing demand for premium dairy products and the increasing importance of cheese exports are reshaping trade flows and creating new opportunities for dairy exporters worldwide.

For dairy processors and exporters, success will increasingly depend on product diversification, value addition and the ability to respond quickly to shifting regional demand patterns as the global dairy market continues to evolve.