Executive Summary

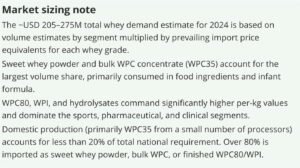

India presents the world’s most striking dairy protein paradox. As the world’s largest milk producer — contributing 24% of global output at 239 million tonnes (MT) in 2023-24, India should theoretically be a major source of whey protein. Instead, it produces less than 20% of its national whey protein requirement domestically, with over 80% of demand across all segments — sports nutrition, pharmaceuticals, nutraceuticals, infant formula, geriatric nutrition, and food ingredients — met by imports of sweet whey powder and bulk WPC concentrate from the EU, New Zealand, and the United States.

- India’s Dairy Landscape

1.1 Milk Production Scale & Growth

5.7% Þ 5.3% Þ 4.4% Þ 3.7% in successive years. Production is forecast to reach ~247–252 MMT by 2025-26, consistent with this trend — earlier estimates of 255–265 MMT implied implausible 8%+ growth and have been revised.

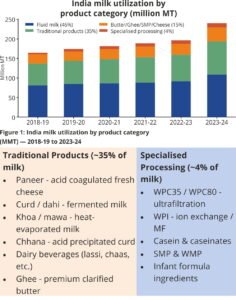

1.2 Milk Utilization by Product Category

The utilization structure of Indian milk differs fundamentally from western dairy nations. Approximately 46% is consumed as fluid

- Western Cheese Production & Sweet Whey

2.1 Western Cheese: Scale Significantly Larger Than Published Estimates

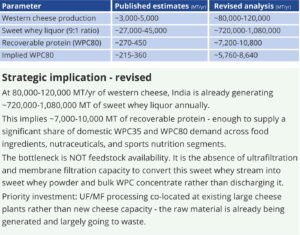

Published FAO statistics place India’s western cheese production at approximately 3,000 MT/yr — a figure that is substantially incorrect. Amul alone operates a 120 MT/day cheese facility (~43,800 MT/yr from a single plant). Parag Milk Foods, Mother Dairy, Karnataka Milk Federation, and other large cooperatives and private processors add significant additional volume. Organised sector production across all major players is estimated at 80,000–120,000 MT/yr, with the true figure pending verification against National Dairy Development Board and Ministry of Animal Husbandry data.

2.2 Sweet Whey Generation — Revised Estimates

- Paneer Whey: The Dominant But Challenging Stream

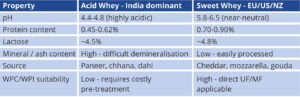

3.1 Scale of Acid Whey Generation

India generates approximately 3 MT of liquid whey annually from paneer and chhana production alone. At a conservative estimate of 3 MT of paneer produced annually (paneer market valued at INR 648 billion in 2024), roughly 9 litres of acid whey is generated per kilogram — yielding ~27 MT of acid whey liquor per year, most of which is discarded or used as animal feed at near-zero value.

3.2 Acid vs Sweet Whey — Why Chemistry Matters

3.3 Valorization Pathways for Acid Whey

While acid whey cannot be directly processed into WPC80/WPI at commercial scale, it holds significant value through alternative routes:

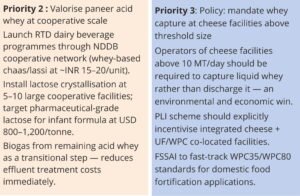

- RTD dairy beverages — whey-based lassi, chaas, flavoured whey drinks. Growing consumer acceptance of functional dairy beverages creates a direct high-volume outlet. NDDB actively promoting cooperative-level bottling.

- Fermentation substrate — acid whey’s lactose and peptide content makes it suitable for yeast and bacterial fermentation, producing bioethanol, lactic acid, and single-cell protein for animal feed.

- Lactose crystallisation — demineralisation followed by evaporation and crystallisation can yield food-grade lactose at USD 800–1,200/tonne for pharmaceutical and infant formula markets.

- Biogas generation — lowest-value pathway but widespread in cooperative dairies; reduces effluent BOD/COD load and generates on-site energy.

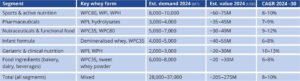

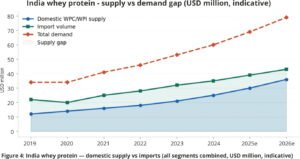

- Protein Supply-Demand Gap

India’s whey protein demand spans six distinct end-use segments, each with different product specifications, price points, and growth dynamics. A common error is to size the market only around the sports nutrition and consumer supplement channel — this substantially understates total

4.2 Import Dependency — The Sweet Whey & Bulk WPC Gap

India’s domestic whey processing capacity is nascent. The country produces less than 20% of its national whey protein requirement domestically. What is being produced is primarily WPC35, with limited WPC80 output from a handful of processors (Amul, Parag Milk Foods, and a small number of cooperative plants).

- European Union (France, Germany, Netherlands, Ireland) — largest source, approximately 55–60% of import volumes

- New Zealand and Australia — approximately 20–25% of imports, strong in WPI and infant-grade ingredients

- United States — historically ~15–20% of imports; access disrupted since November 2024 by veterinary health certificate requirements

It is important to note that when considering waste and underutilisation of India’s whey opportunity,

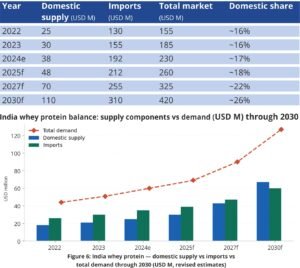

4.4 Quantified Gap — 2022 to 2030

The table below reflects total whey demand across all segments. Domestic production (primarily WPC35) remains below 20% of national requirement through the forecast period under base-case assumptions.

- Industry Response & Key Players

5.1 Cooperative Sector

Amul (GCMMF) operates India’s largest cheese manufacturing facility at 120 MT/day and has launched a comprehensive high-protein product range including whey protein powder priced at approximately INR 2.5 per gram. The scale of Amul’s cheese operation means it generates the largest single sweet whey stream in India. Installing UF/MF processing at this facility to produce sweet whey powder and bulk WPC concentrate rather than discharging the liquid stream represents the single largest domestic whey protein production opportunity in the country.

NDDB is actively promoting co-product valorisation at the cooperative level, including acid whey-based dairy beverage programmes and lactose recovery pilot projects. NDDB’s mandate to improve farmer returns is a structural driver for whey monetisation beyond the animal feed route.

5.2 Private Sector

Parag Milk Foods has established a dedicated whey processing facility in Maharashtra and integrates WPC into both B2C consumer products (Avvatar brand) and B2B ingredient supply. The company expects whey to contribute 15% of revenues within three years — a significant pivot for a traditionally commodity-focused dairy processor.

Godrej Agrovet announced an INR 15,000 million (USD 180 million) dairy processing facility in Telangana in December 2025, signalling major private-sector commitment to fractionation capacity. The scale of this investment implies a protein-centric revenue model.

5.3 Government Policy Support

- PLI (Production Linked Incentive) scheme: reimburses up to 50% of qualifying CapEx for dairy processing investments — directly reduces economics of building UF/MF/WPC plants.

- National Programme for Dairy Development (NPDD): funds cold chain, processing, and quality testing infrastructure at cooperative level.

- Veterinary health certificate (VHC) requirements: from November 2024, US-origin whey requires VHC clearance — creating market space for domestic producers to substitute imports.

Conclusions

Six revised key conclusions for India’s dairy protein trajectory through 2030:

- Western cheese production is far larger than published data suggests. Amul’s 120 MT/day facility alone generates more cheese annually

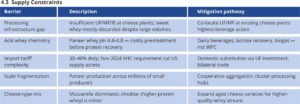

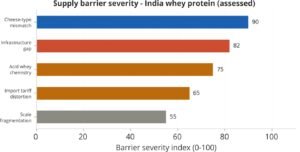

- The bottleneck is processing, not feedstock. India has sufficient sweet whey liquor to be largely self-sufficient in WPC35 and a meaningful WPC80 producer. The gap is ultrafiltration and membrane filtration capacity at cheese plants — a capital investment problem, not a raw material problem.

- Domestic production is less than 20% of national requirement. India currently produces below one-fifth of its total whey protein need across all segments. Over 80% is imported as sweet whey powder and bulk WPC concentrate. This creates acute vulnerability to global price shocks, trade disruptions (as seen with the US VHC requirements in November 2024), and currency depreciation.

- Acid whey valorisation remains India’s unique co-product challenge. The ~27 MT/yr of paneer acid whey cannot be processed into sweet whey-grade WPC, but represents a major opportunity for dairy beverages, lactose recovery, and fermentation. This is a separate stream from the sweet whey generated by western cheese — the latter is where the WPC35 and WPC80 opportunity lies.

- Ghee is a strategic traditional product, not a commodity. It is India’s largest dairy export category and should be recognised as a premium value-added product rather than grouped with commodity dairy outputs.

- India is a major amplifier of the global protein gap. As a large, fast-growing import market drawing on global WPC/WPI supply while not yet contributing to it, India is a critical variable in the Gira 2030 protein gap analysis — and the country with the largest single investment opportunity in dairy protein processing.