Europe’s dairy industry is witnessing a significant market correction as farm-gate milk prices continue to decline amid rising milk production, changing export demand and increasing global competition.

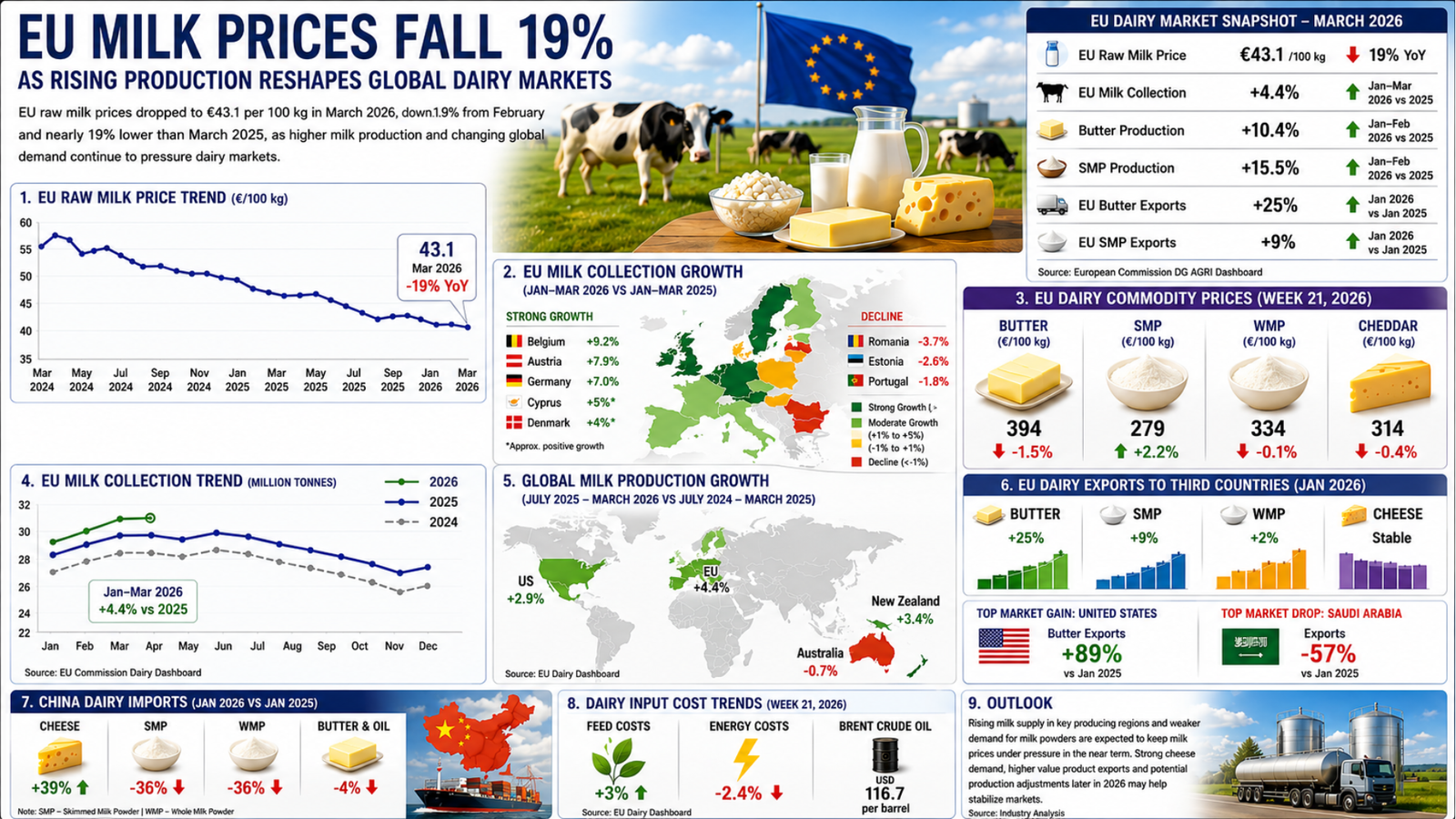

According to the latest European Commission dairy dashboard, the average EU raw milk price stood at 43.1 euro per 100 kg in March 2026, representing a 1.9% month-on-month decline and a sharp 19% fall compared to March 2025.

The downturn reflects mounting pressure from expanding milk supplies across major dairy-producing regions and softer demand for several dairy commodities in international markets.

EU Milk Production Continues to Surge

One of the primary drivers behind falling milk prices has been a strong increase in milk collection across the European Union.

European Commission data shows that EU cow milk collection increased by 4.4% during January-March 2026 compared with the same period last year. The production growth trend has moved significantly above 2024 and 2025 levels, signalling higher milk availability across the bloc.

Countries Reporting Strong Milk Collection Growth

| Country | Growth |

|---|---|

| Belgium | +9.2% |

| Austria | +7.9% |

| Germany | +7.0% |

| Cyprus | Positive Growth |

| Denmark | Positive Growth |

Meanwhile, Romania, Estonia and Portugal registered declines in milk collection during the same period.

The increase in milk supply has intensified pressure on processors and dairy commodity markets, contributing to weaker farm-gate returns for dairy farmers across Europe.

Dairy Commodity Markets Show Mixed Trends

Despite lower milk prices, dairy commodity production remains strong in several categories.

The latest EU market data shows:

| Commodity | Price €/100kg | Trend |

| Butter | 394 | ▼ 1.5% |

| SMP | 279 | ▲ 2.2% |

| WMP | 334 | ▼ 0.1% |

| Cheddar | 314 | ▼ 0.4% |

Production trends during January-February 2026 revealed:

- SMP production increased by 15.5%

- Butter production rose by 10.4%

- Cheese production increased by 2.3%

- Fermented dairy products grew by 2%

At the same time, production declined in categories such as cream, whole milk powder and concentrated milk.

Industry analysts believe processors are increasingly focusing on export-oriented and value-added dairy products in response to evolving global demand patterns.

Global Milk Production Expansion Intensifies Competition

The pressure on dairy markets is not limited to Europe alone.

Milk production has also increased across several major exporting regions:

| Region | Production Growth |

| European Union | +4.4% |

| New Zealand | +3.4% |

| United States | +2.9% |

| Australia | -0.7% |

Comparative pricing data indicates EU milk prices remain higher than competing exporters, with EU milk averaging 43.1 €/100 kg compared to 37.3 €/100 kg in New Zealand and 33.8 €/100 kg in the United States.

This widening price gap could affect the competitiveness of European dairy exports in price-sensitive international markets.

Export Markets Continue to Shift

Global dairy trade dynamics are continuing to evolve as import demand patterns change across major consuming countries.

EU export performance during January 2026 showed:

| Product | Export Trend |

| Butter | ▲ +25% |

| SMP | ▲ +9% |

| WMP | ▲ +2% |

| Cheese | Stable |

The United States emerged as a major growth market for EU butter exports, recording an 89% increase compared to January 2025. In contrast, butter exports to Saudi Arabia declined sharply by 57%.

China’s Dairy Imports Reflect Changing Consumption Trends

China’s dairy import trends also reflected shifting consumer and industrial demand patterns.

China Dairy Import Trends – January 2026

| Product | Trend |

| Cheese | ▲ +39% |

| SMP | ▼ -36% |

| WMP | ▼ -36% |

| Butter & Oil | ▼ -4% |

The figures indicate growing demand for value-added dairy products such as cheese, while imports of milk powders continue to soften.

This trend could significantly influence future dairy trade strategies among major exporting regions, including Europe, New Zealand and the United States.

Feed and Energy Costs Remain Volatile

Even as milk prices decline, dairy producers continue facing uncertainty around input costs.

According to the EU dashboard:

- Feed costs increased by 3%

- Energy costs declined by 2.4%

- Brent crude oil remained elevated at USD 116.7 per barrel

The combination of lower milk prices and fluctuating production costs is creating fresh profitability concerns for dairy farmers throughout Europe.

Outlook for the European Dairy Sector

Analysts believe the EU dairy market could remain under pressure in the near term as milk production growth continues to outpace demand recovery.

However, relatively stable cheese demand, stronger butter exports to select destinations and potential production adjustments later in 2026 may help moderate further declines in milk prices.

The latest market developments underline the increasingly interconnected nature of global dairy trade, where production growth in one region can rapidly influence international milk prices, export competitiveness and farmer profitability worldwide.

For the global dairy industry, the current correction highlights the ongoing challenge of balancing production expansion with sustainable market demand.