📈 Farm-gate milk prices across the European Union have surged to their highest level in over a decade, driven by constrained production, seasonal demand, and policy-related investment hesitation. The impact is being felt unevenly across member states, exposing structural imbalances in Europe’s dairy supply chain.

📊 A Historic High: EU Average Tops €0.53/kg

In April 2025, the average EU farm-gate milk price reached €0.53/kg, representing a 13% year-on-year increase. This bullish trend continued into June, with upward pressure sustained by regional supply deficits and strong downstream demand, particularly in the cheese and value-added segments.

🚜 What’s Driving the Price Surge?

According to dairy market analysts and EU monitoring reports, the current price rally is supported by four critical forces:

1. 📉 Constrained Supply from Disease and Drought

Ongoing bluetongue outbreaks, weather shocks, and stringent nitrate regulations in countries such as the Netherlands and Belgium have depressed production volumes. A projected 0.2% decline in EU milk output for 2025 underscores the structural nature of the tightening.

2. 🌞 Seasonal Uplift in Demand

As summer ramps up, so does demand for butter, cream, and ice cream, particularly in tourism-heavy regions such as Southern Europe. This intensifies local shortages, elevating prices in net-deficit countries.

3. 💶 Input Cost Inflation

Feed prices remain elevated due to global supply constraints. Additionally, energy and labour costs across Europe have skyrocketed. For many small- and mid-sized farmers, rising operational costs have offset much of the gains from higher milk prices.

4. 🏛️ Policy Paralysis Stifling Investment

Major processors and farmer cooperatives cite regulatory uncertainty—especially around the EU’s evolving climate goals—as a barrier to capital expansion. Arla Foods’ CEO recently warned that “green rules without clarity are making long-term investment risky” (Financial Times, FT.com).

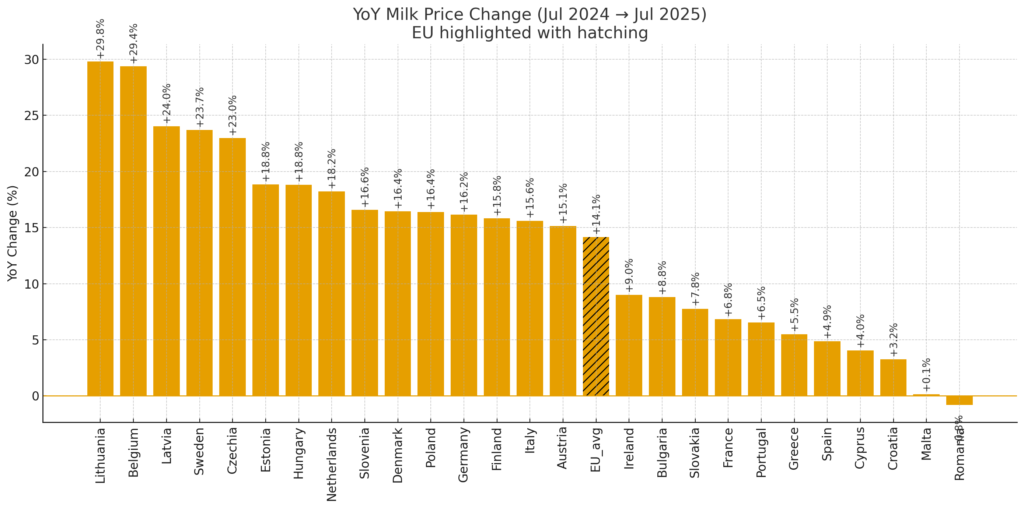

🌍 Regional Disparities: Not All Milk Is Valued Equally

While the EU average price paints a bullish picture, the situation varies widely between member states. Some countries are experiencing explosive growth in farm-gate prices, while others show only marginal improvement.

📋 Comparative Table: April/June 2025 vs MoM and YoY

| Country | Price (€/kg) | MoM Change | YoY Change | Key Drivers |

|---|---|---|---|---|

| Sweden | €0.56 | +2.5% | +33.0% | Tight local supply, high processing costs |

| Lithuania | €0.52 | +1.9% | +29.8% | Strong export demand, herd decline |

| Ireland | €0.54 | +1.2% | +24.0% | Cheese demand, seasonal surge |

| Netherlands | €0.55 | +1.5% | +15.4% | High-value dairy, stable demand |

| Germany | €0.53 | +1.0% | +12.3% | Moderate supply tightening |

| France | €0.51 | +0.8% | +10.2% | Steady consumer demand |

| Poland | €0.48 | +0.7% | +8.5% | Input costs are moderating growth |

| Spain | €0.50 | +0.5% | +3.0% | Overcapacity, less price momentum |

| Croatia | €0.47 | +0.4% | +2.1% | Stagnant output, small market |

| Cyprus | €0.46 | +0.3% | +4.0% | Import-reliant, slow rebound |

| EU Average | €0.53 | +1.3% | +15.0% | – |

📌 Insight: The strongest YoY increases were seen in Sweden, Lithuania, and Ireland, while Southern Europe—including Spain and Cyprus—lags behind due to structural oversupply and slower product diversification.

🧠 Strategic Implications for Dairy Stakeholders

🐄 For Dairy Farmers:

- Short-term margins improve, but cost pressures continue to be a drag.

- Climate policy clarity is essential to justify herd expansions or facility upgrades.

🧀 For Processors:

- Opportunities lie in high-value segments (cheese, protein concentrates).

- Supply chain risks must be mitigated with diversified sourcing and longer-term contracts.

🧭 For Policymakers:

- Investment in alternative protein feed can reduce reliance on imports and stabilise producer costs.

- Clear, phased environmental rules will help unlock CAPEX across the value chain.

🔚 Conclusion: Boom or Breaking Point?

The EU dairy sector is riding a historic price wave, but beneath the surface lie serious concerns: investment reluctance, environmental compliance stress, and a fragile feed supply system.

If these issues are not addressed proactively, today’s price surge could be a temporary peak rather than a platform for stable, sustainable growth.

🧭 For the dairy sector to truly capitalise, the EU needs a coordinated strategy: clear green policies, investment in protein independence, and support for modernising supply chains.