As India transitions into FY 2024-25, its economic trajectory remains robust yet fraught with challenges. The nation is one of the world’s fastest-growing economies, supported by government-led deregulation, infrastructure investment, and expanding industrial capacity. However, inflationary pressures, geopolitical uncertainties, and global trade fluctuations cast shadows over sustained growth. This critical analysis evaluates India’s economic progress, industrial development, and the transformative shifts in the dairy sector, incorporating insights from the Economic Survey 2024-25.

Economic Growth: A Strong Yet Cautious Expansion

India’s GDP is forecasted to grow 6.4% in FY25, underpinned by private consumption, rural demand recovery, and infrastructure-driven investments. While global growth remains sluggish at 3.2% in 2024 and 3.3% in 2025, India’s internal dynamics provide resilience.

Private consumption, which accounts for 60% of GDP, remains the linchpin of economic activity. Previously dampened by inflation, rural demand is rebounding due to higher agricultural yields and government stimulus. FMCG, consumer durables, and retail are poised for expansion, driven by festive and discretionary spending.

Government capital expenditure (capex) continues its upward trend, focusing on roads, railways, and digital infrastructure. Private sector participation in manufacturing and services benefits from PLI incentives, tax reforms, and ease-of-doing business initiatives. With global inflation stabilising, India’s interest rate environment remains conducive to growth. However, food price volatility remains a concern, warranting continued monetary vigilance by the RBI.

Government capital expenditure (capex) continues its upward trend, focusing on roads, railways, and digital infrastructure. Private sector participation in manufacturing and services benefits from PLI incentives, tax reforms, and ease-of-doing business initiatives. With global inflation stabilising, India’s interest rate environment remains conducive to growth. However, food price volatility remains a concern, warranting continued monetary vigilance by the RBI.

Global geopolitical conflicts and the EU’s Carbon Border Adjustment Mechanism (CBAM) could affect export-oriented industries. Trade diversification and policy adaptations are crucial for maintaining India’s export competitiveness.

Industrial Sector: Structural Challenges & Opportunities

India’s industrial sector is projected to grow at 6.2% in FY25, bolstered by infrastructure, energy, and manufacturing expansion. Domestic demand sustains manufacturing growth, while weak external markets limit exports. Pharmaceuticals, electronics, and textiles leverage supply chain localisation and export diversification. EV manufacturing and semiconductor production are gaining momentum.

Employing 12.41% of the organised workforce, food processing is pivotal to employment and rural stability. Government initiatives like PMKSY and PLI schemes bolster sectoral investments. Public sector investments drive demand for steel and cement, but energy costs and raw material volatility persist as challenges.

The automobile sector has seen a 12.5% rise in domestic sales, indicating strong consumer interest in EVs and hybrids. PLI incentives and domestic battery production enhance the industry’s sustainability. In the electronics sector, 99% of smartphones sold in India are domestically manufactured, and India’s semiconductor ambitions are materialising through foreign investments and policy support.

Dairy Sector: A Pillar of Rural Economic Growth

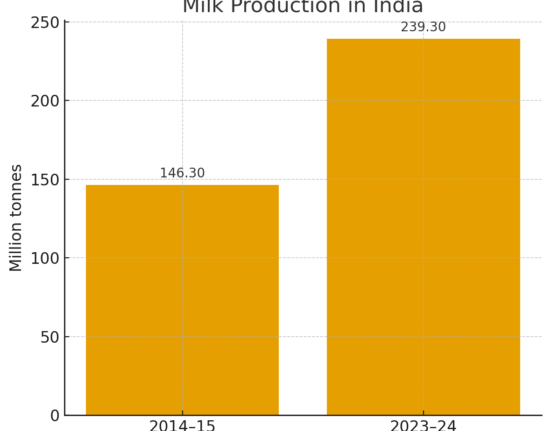

The dairy industry is shifting from high-volume production to high-value-added products, enhancing profitability and global competitiveness. Livestock contributes 30.23% to agricultural GVA, up from 24.38% in FY15. The dairy sector’s economic contribution reached тВ╣11.16 lakh crore ($133.16 billion) in FY23, with a CAGR of 12.99%, reflecting rapid expansion and modernisation.

Government initiatives are significantly shaping the sector’s growth. The Rashtriya Gokul Mission focuses on enhancing indigenous breed productivity, while the MAITRIs Program has inducted 38,736 AI technicians to improve livestock breeding services. Financial support measures include the establishment of over 9,000 dairy cooperatives, which are expanding market access.

Consumer preferences are shifting towards premium dairy products such as cheese, yoghurt, probiotics, and flavoured milk. Cold chain infrastructure and logistics modernisation are crucial for minimising wastage and ensuring quality compliance. However, challenges such as high input costs, inefficiencies in cold storage infrastructure, and regulatory hurdles in the export market persist, necessitating strategic policy interventions.

Outlook for 2024-25: Key Takeaways

India is projected to maintain one of the highest global growth rates, but external risks require policy vigilance. Reducing dependence on imported raw materials (semiconductors, EV batteries) is a strategic focus. Government incentives will continue to bolster domestic manufacturing competitiveness.

Increasing milk production and cooperative networks will support rural economic sustainability. Investments in cold chain logistics and high-value dairy processing are critical for enhancing profitability.

Conclusion: A Year of Structural Transformation

India’s economic and industrial landscape is poised for steady growth, underpinned by domestic consumption, infrastructure development, and policy-driven manufacturing incentives. However, uncertainties such as geopolitical conflicts, supply chain disruptions, and climate-related risks necessitate a dynamic and adaptive policy framework.

Enhancing value-added production, cooperative strength, and supply chain efficiency for the dairy sector will be pivotal in maintaining global competitiveness and long-term sustainability.