🌍 Global Dairy Markets Face Crosswinds as China Contracts and Trade Wars Escalate

March 26, 2025 | Dairy Dimension – Global Markets Desk

While global dairy exporters are preparing for a modest rebound in 2025, China—the world’s most strategically watched dairy market—is contracting. A new report from RaboResearch forecasts a 2.6% decline in Chinese milk production in 2025, marking the second straight year of shrinkage after a prolonged period of growth.

At the same time, Beijing is stepping in with economic stimulus signals, including a rare high-level meeting between President Xi Jinping and dairy sector leaders, hinting at domestic demand activation through policy intervention.

📉 China’s Dairy Retreat: A Structural Shift?

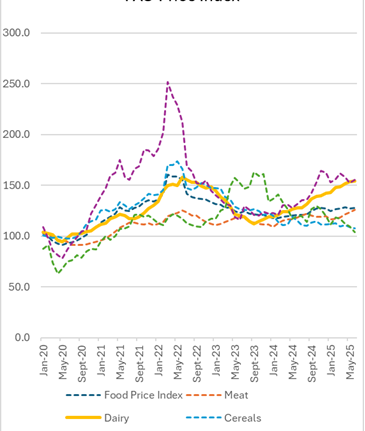

The data is sobering:

- Farmgate milk prices in China are down 15% year-over-year (Feb 2025)

- Margins are squeezed, expansion is stalled, and farmer sentiment is low

- Rabobank suggests this downturn is cyclical, but not temporary

China’s shrinking production has global implications. As the world’s second-largest dairy importer, even small shifts in Chinese demand can tilt global prices, trade routes, and strategy.

🌐 Exporters on the Rise: US, EU, NZ, and the Cost of Growth

While China slows down, other dairy powerhouses are scaling up:

- EU and US production is forecast to rise modestly, supported by lower feed costs and resilient export demand

- New Zealand is entering a bullish phase, riding record milk prices and the highest farmer confidence in a decade

“Spring 2025 peak production in NZ will be a bellwether for global price momentum,” notes Rabobank.

However, increased global supply may face resistance, not from production issues—but from politics.

⚠️ Trade Wars: The New Dairy Disruptor

The stability of global dairy trade is now under siege, with the US–China and EU–China tensions taking center stage.

China’s Tariff Retaliation (effective March 10, 2025):

- 10% duty on US dairy, pork, soy, beef, fruit, seafood

- 15% on grains and poultry

US dairy exports to China (42% of its whey exports) and Mexico (cheese exports up 30% YoY) could take a hit, threatening farmgate milk prices and dampening optimism in the US Midwest.

Simultaneously, China is investigating European dairy subsidies in retaliation for EU tariffs on Chinese EVs. A decision is expected in early 2026, possibly reducing EU access to one of its largest export markets.

📉 India’s Watch Zone: Strategic Implications for South Asia

Although India is not a major dairy exporter, these shifts hold strategic relevance:

- Global price volatility could influence India’s SMP (skimmed milk powder) stock strategies and buffer procurement timing

- EU and US surpluses may seek alternate buyers in South Asia, leading to price competition

- India’s A2, organic, or indigenous-focused dairy brands may find opportunities in markets looking for non-commoditized offerings

Moreover, India must monitor tariff movements, trade blocs, and disease alerts, especially if looking to participate more in international dairy trade in the next decade.

🌎 Other Market Movers to Watch

🇦🇷 South America:

-

Strengthening Argentine peso may divert dairy from exports to domestic markets, altering regional trade flows.

🇪🇺 Europe:

-

Disease risk is rising, with bluetongue re-emerging and FMD (foot-and-mouth disease) recently detected and contained in Germany—posing logistical and cost uncertainties.

🧠 Analyst Take: 2025 Will Test Dairy’s Agility, Not Just Its Output

This year is not about producing more milk—it’s about navigating a multipolar, volatile world:

- China is rebalancing

- The US is contesting trade

- The EU is watching for biosecurity threats

- Latin America is dealing with currency chaos

And in the middle of this, India sits with a self-sufficient dairy model, buffered (for now) but needing forward-looking risk intelligence to anticipate shifts, especially in commodity prices and dairy ingredient demand.