From the world’s largest milk producer to a credible global dairy exporter

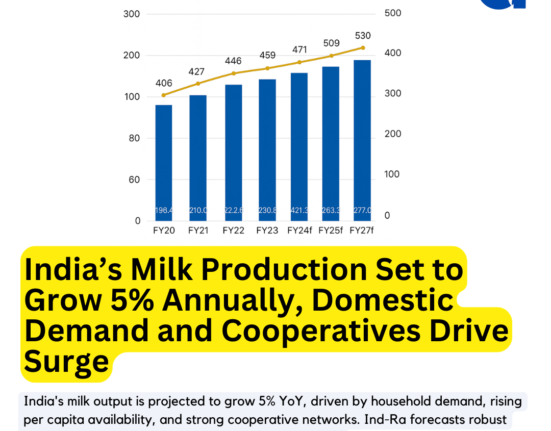

India’s dairy sector has long been defined by scale. With annual milk production exceeding 239 million tonnes, the country has retained its position as the world’s largest milk producer for over two decades. It supports the livelihoods of more than 80 million farmers, underpins national nutrition security, and represents one of the most resilient segments of Indian agriculture.

Yet, for all its scale, India remains a marginal player in global dairy trade.

This contradiction—dominance in production but insignificance in exports—is now at the centre of the sector’s next transformation. As outlined in a recent analysis by Jordbrukare India’s Dairy Market Intelligence (March 2026), India is entering a decisive phase where production growth, demand evolution, and policy direction are converging to reshape its global positioning.

The Scale Advantage—But Not Yet a Competitive Edge

India’s dairy growth trajectory is unmatched. Over the past decade, milk production has expanded at a compound annual growth rate of over 5.6%, significantly outperforming the global average of around 1.5%.

Per capita availability has risen to 471 grams per day, comfortably exceeding recommended nutritional thresholds. The domestic dairy market, already valued at approximately USD 228 billion, continues to expand at double-digit rates.

However, scale alone has not translated into competitiveness.

India’s dairy system remains structurally fragmented, with smallholder farmers having limited access to consistent veterinary services, high-quality feed, and productivity-enhancing technologies. As a result, average milk yields remain at ~5.3 kg per animal per day, far below global benchmarks.

This productivity gap is not just a technical constraint—it is the single most important determinant of India’s cost structure and export competitiveness.

The Export Paradox: A Structural Missed Opportunity

Despite contributing nearly 25% of global milk production, India accounts for less than 0.3% of global dairy trade by value.

Even with recent momentum—exports rising to an estimated USD 490 million in FY 2024–25—India remains a minor participant in international markets.

The contrast is stark:

- New Zealand, with less than one-tenth of India’s milk production, exports over USD 14 billion worth of dairy annually

- India, despite its scale, remains largely inward-focused

The reasons are structural and persistent:

- Low farm-level productivity

- Limited cold chain penetration

- Narrow export product mix dominated by butter and ghee

- Inconsistent policy signals around agricultural exports

As highlighted in the Jordbrukare analysis, India’s challenge is not demand—it is the ability to convert surplus milk into export-grade, value-added products at scale.

A Structural Demand Shift Is Underway

While export competitiveness remains underdeveloped, domestic demand is undergoing a significant transformation.

India is experiencing a dietary transition, driven by rising incomes, urbanisation, and changing consumer preferences. Consumption is steadily shifting from staple carbohydrates toward high-value, protein-rich foods, with dairy at the centre of this shift.

This is reshaping the market in two important ways:

- Premiumisation of dairy consumption

Urban consumers are increasingly demanding products such as cheese, Greek yoghurt, protein-enriched milk, and functional dairy beverages. - Growth of value-added segments

These categories command significantly higher margins—often 2 to 5 times that of liquid milk—and are growing faster than overall dairy consumption.

The implication is clear:

👉 India’s dairy future will be defined less by volume growth and more by value creation.

Export Momentum: Early Signals from the Gulf

India’s dairy export story is beginning to take shape, particularly in the Middle East (GCC).

Recent trends indicate:

- A sharp rise in butter exports (+600% over five years)

- Strong demand from Saudi Arabia, UAE, and Bahrain

- Increasing competitiveness driven by India’s milk surplus and pricing advantage

However, India’s current export basket remains heavily skewed toward commodity dairy fats, with limited presence in premium categories such as cheese, whey proteins, and specialised dairy ingredients.

This creates a strategic vulnerability.

Global competitors—including New Zealand, Australia, and the European Union—continue to dominate high-value segments, supported by strong branding, quality consistency, and long-term buyer relationships.

India’s window of opportunity is real—but it is also time-bound.

Productivity: The Central Lever for Transformation

If there is one variable that will determine India’s dairy trajectory over the next two decades, it is productivity.

At present, India’s average yield of ~5.3 kg per animal per day is less than one-third of global benchmarks. Bridging even part of this gap would have transformative effects:

- Lower cost of production

- Higher farmer incomes

- Improved export competitiveness

- Reduced emissions intensity per litre of milk

Notably, India’s climate strategy reinforces this direction. The NITI Aayog’s Net Zero pathway identifies productivity improvement as the single most effective intervention—aligning growth, sustainability, and income objectives.

In effect, the sector’s economic and environmental goals are converging.

Infrastructure: The Missing Link

A structural imbalance marks India’s dairy ecosystem:

- Milk production is concentrated in northern and central states

- Processing and organised infrastructure are stronger in the western and southern regions

This mismatch limits the efficient movement of milk into value-added channels and export markets.

Moreover, less than 5% of milk in India is transported under refrigeration, severely constraining the ability to build export-grade supply chains.

Bridging this gap will require:

- Expansion of cold chain infrastructure into production-heavy regions

- Investment in decentralised processing capacity

- Integration of quality-based procurement systems

Government initiatives such as the Animal Husbandry Infrastructure Development Fund (AHIDF) are a step in the right direction—but execution will be critical.

A Converging Industry Structure

India’s dairy sector is entering a new phase of structural evolution.

The cooperative model—led by organisations such as Amul—has been instrumental in building scale and ensuring farmer participation. However, the next phase of growth will increasingly depend on the private sector’s ability to drive innovation, branding, and value addition.

Recent investments by companies such as Britannia, Lactalis, and regional dairy players signal a shift toward:

- Higher processing capacity

- Expansion into premium categories

- Greater focus on export markets

The future of Indian dairy will likely be defined by a hybrid model in which cooperatives and private players operate in complementary roles.

The Road to 2047: A Strategic Choice

India’s dairy sector is not constrained by demand. It is not constrained by production.

It is constrained by the ability to translate scale into competitiveness.

As Jordbrukare India’s analysis underscores, the country is structurally positioned for export-led growth, with a sustained surplus projected through 2047.

The question is not whether India will grow—it will.

The real question is:

👉 Will India remain a low-margin, domestic-focused dairy economy, or evolve into a global, value-added dairy powerhouse?

Conclusion: From Potential to Positioning

India’s dairy sector stands at a strategic crossroads.

The fundamentals are strong:

- Unmatched production scale

- Growing domestic demand

- Emerging export opportunities

But realising this potential will require coordinated action across:

- Productivity improvement

- Cold chain and processing infrastructure

- Export policy stability

- Value-added product development

The next decade will determine whether India can move beyond being the world’s largest milk producer to becoming one of its most influential dairy exporters.

For processors, investors, and policymakers, the message is clear:

👉 The time to build for global markets is now.

Source: Jordbrukare India – Dairy Market Intelligence Report, March 2026

Request Access at: info@jordbrukare.com